Green Wick · The Signal Lab

Finding one signal worth paying for.

A working page, not a product.

The goal: use AI to surface correlations humans miss, distil them into a reliable, frequently-firing, tradable signal, prove it the disciplined way — backtest → private forward-proof → public track record — and only then charge for it. This page is the live workbench where we narrow an impossibly wide search down to the one thing we actually ship.

00The premise — is this even possible?

Yes — but only the disciplined, narrow version.

The category is proven: quant funds, paid signal groups, alt-data shops and prediction-market models all sell predictions for real money. We don't even need to beat the market for our own book — we need a track record convincing enough that people subscribe. That is a slightly lower bar than running a fund, but it is reputationally unforgiving.

- Inefficient corners exist — retail-driven, under-covered, brand-new markets.

- Edges live in rare data + patient horizons, not in latency we can't afford.

- Even a modest persistent edge is monetizable as a subscription.

- Cost to try is low: the data infra and compute already exist here.

- Markets are mostly efficient. Obvious signals are already arbitraged away.

- Overfitting is the #1 killer — feed AI 1,000 series and it will find gorgeous backtested noise.

- Edges decay once crowded. A signal that works gets copied.

- The real risk isn't "can't find one" — it's shipping an overfit one and burning trust.

★The truths most signal sellers hide

The reasons this is hard are exactly the reasons ours will be different.

- Markets are mostly efficient. The obvious signals are already arbitraged away. What's left is small, hard-won edges that decay once crowded.

- The #1 killer is overfitting: give AI thousands of data series and it WILL find gorgeous backtested correlations that are pure noise. 95% of "signals" are this. The graveyard is enormous.

- So the discipline (out-of-sample, walk-forward, cost-adjusted, multiple-testing correction, forward-proof BEFORE any public claim) isn't optional — it IS the game.

◇Where we start — distil, don't search

We don't search all of finance from zero. We refine the edges our own systems already hint at.

We've attacked "find signal" three times. They're the same hunt at different resolutions — and this one is the refinery.

Pangle

Many agents collaborate → emergent signal. Wide, decentralized.

Monad wallet-watch

Many strategies × dynamic on-chain data → ensemble signal. Live, noisy, partial wins.

Signal Lab

Distil ONE legible, proven signal. The refinery for the others' hints.

Three opening moves

- Mine our own systems first. Start from signals already showing life — Monad's wallet flags have partial success, and variance in a partial win hides a real edge. Refine, don't rediscover.

- Catalog observable cause → effect. List forced/behavioural flows we can see on-chain before price moves — exchange inflows, token unlocks, liquidation cascades, treasury/bridge moves, smart-wallet accumulation. Rank by edge × data-quality × frequency.

- Run the portfolio through the harness. Every thesis = one screen; out-of-sample is judge; every shot logged; survivors graduate to forward-proof.

01What counts as "a signal worth paying for"

Define the target before searching, or every pretty backtest looks like a winner.

A signal isn't "it went up after X." It is a claim that clears six gates at once. We write these down first so the search has a finish line.

| Gate | The bar | Why |

|---|---|---|

| Reliability | Positive edge per fire, net of costs, with a hit-rate or expected-value that holds out-of-sample. | Subscribers feel losers fast; the edge must survive honesty. |

| Frequency | Fires often enough to matter — think weekly-ish, not once a year. | Rare fires = no statistical proof and no reason to subscribe. |

| Tradability | The instrument is liquid and executable; edge > fees + slippage + impact. | A "signal" you can't act on net-positive is a chart, not a product. |

| Persistence | Survives walk-forward, multiple regimes, and a year of decay. | One lucky window is the overfit trap wearing a suit. |

| Capacity | Enough room that a group acting on it doesn't kill it. | Subscribers are the crowding risk. |

| Mechanism bonus | A plausible reason it exists (forced flows, behaviour, structure). | A "why" is the single best defence against overfitting. |

The scoreboard we'll rank candidates on

# a signal firing weekly with a small clean edge beats a huge edge that fires twice a year

02The search space

The breadth is enormous. Decompose it into axes so we can narrow deliberately, not randomly.

Every candidate signal is one point across five axes. Naming the axes turns "anything in any market" into a finite map we can prune.

A · Target — what we predict

Absolute direction is the hardest and most-mined target. Relative value (A vs B, market-neutral) and volatility are structurally more predictable — we bias here.

B · Arena — where we trade

| Market | Inefficiency | Our data edge | Verdict |

|---|---|---|---|

| Crypto on-chain / DEX | High (retail, 24/7, manipulated) | Strong — multichain flow infra | hunt here |

| Prediction markets (Polymarket/Kalshi) | High (thin, news-driven) | Strong — realtime infra exists | hunt here |

| Crypto social / sentiment | Medium-high | Strong — alphalens | hunt here |

| Equities / FX / commodities | Low (efficient, covered) | Weak — costly data, no latency | deprioritize |

"Out of crypto" sounds like diversification but is actually harder for us: more efficient markets, less rare data. The asset-agnostic ambition is right; the realistic first hunting ground is crypto-native + prediction markets where our data is rare.

C · Source — the input that carries the edge

Most-mined, weakest residual edge. Use as a feature, never the thesis.

On-chain flows, social velocity, search/news, funding/basis. Where rare data still pays.

One market reliably leads another (BTC→alts, majors→long-tail).

Order flow, funding dislocations, forced rebalances/expiries.

D · Horizon — the latency-free zone

We cannot win sub-second (no co-location, no HFT stack). We hunt hours → weeks, where the edge is in what we see and how we reason, not how fast we click.

E · Edge type — why the inefficiency exists

Behavioural (retail over/under-reaction) · Structural (forced flows, expiries, rebalances) · Informational (alt-data others ignore) · Risk-premium (paid to hold a risk). A candidate with no identifiable type is probably noise.

03Where our edge actually concentrates

The intersection of three circles — that's where we dig first.

Market inefficiency

Retail-driven, under-covered, new, manipulated — where edges still exist.

Rare data we hold

Multichain on-chain flows, mempool, DEX/CEX basis, social sentiment, prediction-market books.

Latency-free horizon

Hours-to-weeks, so we never race infrastructure we don't have.

04The anti-overfitting discipline

This isn't a section of the method. It IS the method. Break these and we ship noise.

- Hypothesis-first, not mining-first. Start from a mechanism ("forced sellers around X cause Y"), then test it. Pure data-dredging across thousands of series guarantees false positives.

- Train / validate / lockbox. A holdout slice is touched once, at the very end. If we peek, it's contaminated and worthless.

- Walk-forward, not single backtest. Roll the window forward through time; a signal must keep working on data it was never fit on.

- Cost-real from the first number. Every backtest is net of fees, slippage, market impact, and borrow. Gross edge is a fantasy.

- Penalise the search. Track how many ideas we tried; apply a multiple-testing / deflated-Sharpe haircut. Twenty shots will produce one "winner" by luck alone.

- Regime test. Bull, bear, chop, and at least one crisis window. An edge that only works in one regime is a beta in disguise.

- Forward-proof before any claim. Paper-trade it live, privately, before a single public post. The backtest earns the right to a forward test; the forward test earns the right to go public.

- The "already arbitraged?" check. If it's obvious and easy, the edge is gone. Ours must rest on data breadth or compute others don't apply.

05The funnel — from infinite ideas to one shipped signal

Eight gates. Most candidates die early and cheaply. That's the point.

06Hypothesis backlog

Concrete, mechanism-based starting bets. Each is a falsifiable claim, not a vibe.

Seed list — to be tested, killed, or promoted through the funnel. A hypothesis earns a row only if it names a mechanism, the data we already hold, and the exact target.

| # | Hypothesis | Mechanism / why | Data we hold | Target |

|---|---|---|---|---|

| H1 | Stablecoin exchange-inflow surges precede short-horizon majors downside. | Coins moving to CEX = intent to sell (structural/behavioural). | On-chain flow infra | BTC/ETH direction, 6–48h |

| H2 | Smart-money wallet accumulation clusters precede token outperformance. | Informed flow leads price (informational). | Wallet trackers, smart-money poller | Token vs basket, days |

| H3 | Funding/basis dislocations (CEX-perp vs DEX-spot) mean-revert. | Crowded leverage gets paid to unwind (structural). | Multichain price + funding | Spread reversion, hours |

| H4 | Social sentiment-velocity spikes lead short-horizon moves. | Attention precedes flow (behavioural) — must filter manipulation. | alphalens TG/X analyzer | Direction/vol, hours |

| H5 | Polymarket price vs news-velocity diverges, then converges. | Thin books lag breaking information (informational). | Polymarket realtime infra | Event price convergence |

| H6 | BTC regime shift → alt-rotation timing is predictable. | Capital rotates majors→long-tail on a lag (cross-asset lead-lag). | Multichain price feeds | Alt-basket relative, days |

| H7 | Disclosed insider/political trades (Congress, Form 4, 13F whales) — test for RESIDUAL edge after the obvious copy-trade decayed. | Informed actors trade on non-public edge; mandatory disclosure exposes the footprint. Obvious version is crowded (see graveyard) — residual edge, if any, is in faster ingestion or less-covered filings (informational). | Free public filings (STOCK Act, SEC EDGAR) | Named equity, days–weeks |

None of these is "the signal" — they are the first batch to run through §05. Expect most to die at Stage 4. The survivors are what we forward-proof.

A second vector — public claims to test

Thousands publicly claim signals work; almost none publish an out-of-sample test. We harvest the claim and run our gauntlet — the kills feed the graveyard, and once in a while a real one survives. Full catalog in the lab; the priority queue:

| # | Public claim | Arena | Skeptic prior | Data |

|---|---|---|---|---|

| H8 | Overnight vs intraday — the equity premium accrues overnight, not in the session | equities | robust, widely replicated | have |

| H10 | Pre-FOMC drift — S&P ~+49bps in the 24h before FOMC | equities | decayed post-2015 — a live decay test | have |

| H11 | Funding-rate extremes → mean reversion — crowded leverage unwinds | crypto perps | structurally real; strongest of the set | free (Binance) |

| H12 | MVRV / NUPL bands mark cycle tops & bottoms | crypto | real but fires ~yearly → frequency fail | free |

| H13 | Fear & Greed contrarian — fade extreme greed | crypto | weak, widely known | free |

The product angle: publishing "we tested famous signal X and it's dead" is rarer and more trustworthy than another channel shouting buys.

▸Lab log — real runs, kills included

The honest record. Every screen logged, especially the ones that died.

Engine: signal-lab/ — free daily Binance data (12 assets, ~1000 days), a reusable harness with the §04 discipline baked in (time-ordered train/OOS split, cost-real, separate in-sample vs out-of-sample metrics, a persistent multiple-testing counter). A signal earns a forward-test only by clearing out-of-sample.

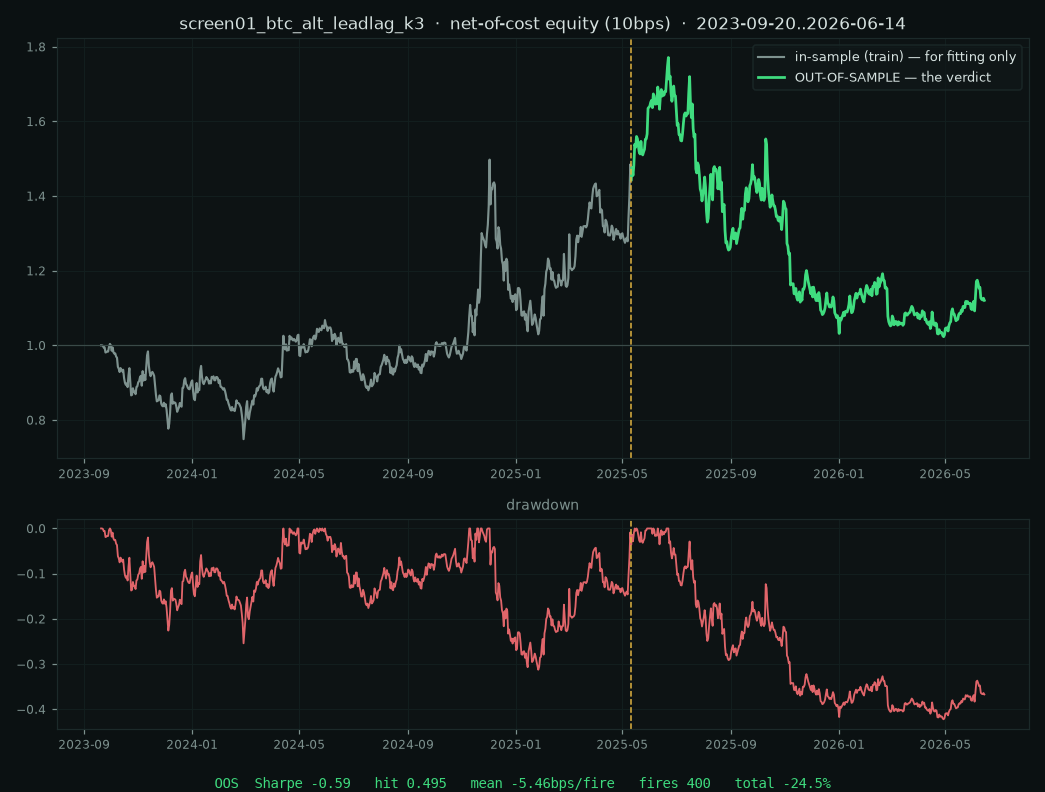

Screen 01 — BTC→alt-basket lead-lag (H6 family)

killed · 2026-06-14Pre-registered: sign of BTC's k-day return predicts the alt basket outperforming BTC the next day (relative-value target, 10bps cost, 60/40 train/OOS). Tested a pre-set family k∈{1,3,7} — no cherry-picking.

| k | In-sample Sharpe | OUT-OF-SAMPLE Sharpe | OOS hit-rate | OOS bps/fire |

|---|---|---|---|---|

| 1 | −0.36 | −0.74 | 0.470 | −6.92 |

| 3 headline | +0.82 | −0.59 | 0.495 | −5.46 |

| 7 | +0.24 | −0.43 | 0.500 | −4.01 |

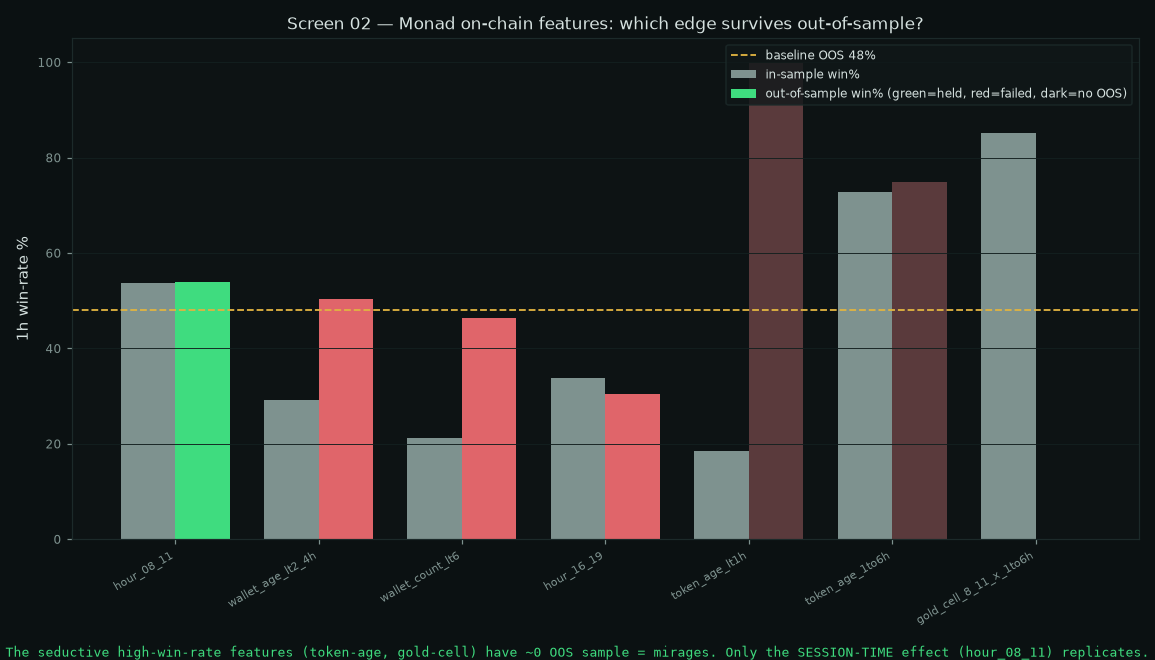

Screen 02 — Monad's invariant (mining our own system)

inconclusive · 2026-06-14Instead of a new backtest, we read what the Monad wallet-bot already proved — its own out-of-sample validation (172k in-sample vs 74k OOS buys). Which on-chain feature actually survives OOS?

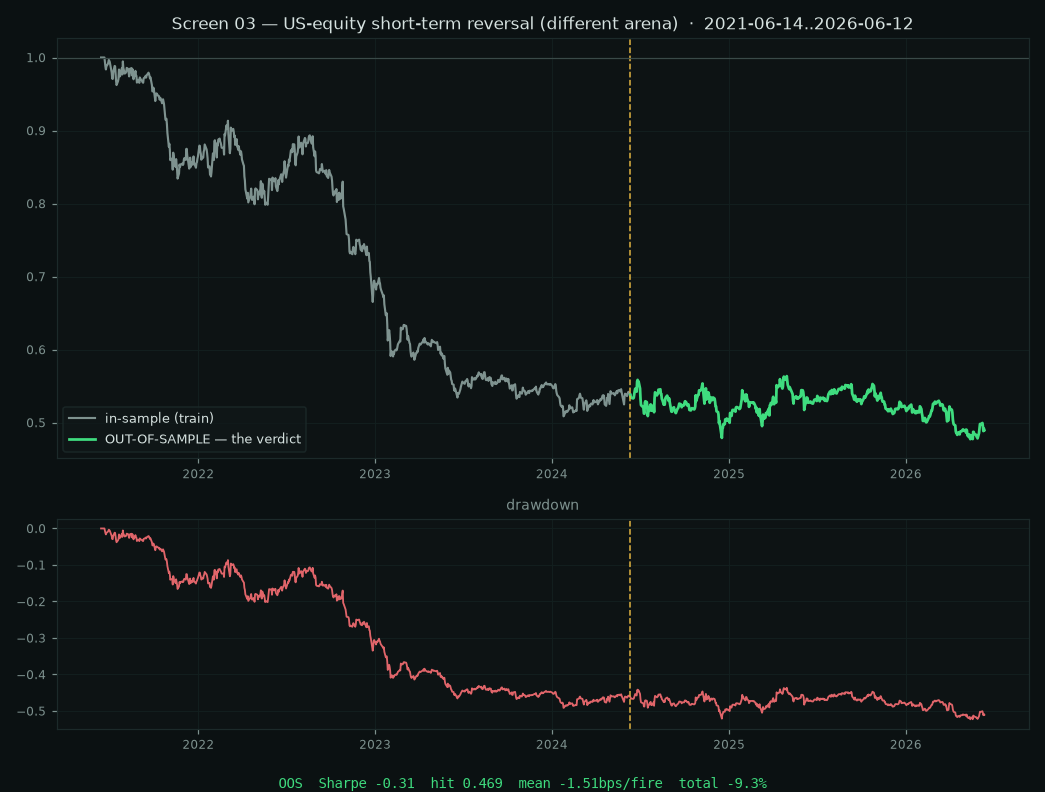

Screen 03 — US-equity short-term reversal (different arena, in parallel)

killed · 2026-06-14Run deliberately in parallel with the Monad mine, in a different arena, so we don't lock into one thing. Dollar-neutral long-losers / short-winners on 15 large caps, 5-day lookback, cost-real.

Screen 04 — fade funding-rate extremes (H11 · the strongest public claim)

killed · 2026-06-14The textbook crypto claim: very positive funding = crowded longs → fade for the reversion. First pass on 66 days looked like a clear winner (OOS Sharpe +1.76). We didn't trust it. Pulling the full 3.5 years (3,150 trades) killed it: Sharpe −0.32, −39%, negative every year since 2023.

07Open questions & parking lot

- What's the minimum public track-record length before charging is honest — 30 fires? 90 days? Both?

- Single flagship signal vs a small basket — basket smooths variance but dilutes the "one special thing" story.

- How do we price capacity so subscribers don't crowd out the edge they're paying for?

- Backtest data sourcing per hypothesis — what history do we have vs need to assemble?

- Manipulation defence for any social-derived signal (H4) — adversaries can spoof the input.

- Where exactly does "AI finds correlations humans miss" add value vs a human with the same data — feature discovery? regime detection? breadth of search? (This is the actual product thesis — sharpen it.)

- Longevity / decay — every edge has a half-life. How do we estimate it before going live, and build a decay-monitor that flags erosion early so we retire a signal before it embarrasses us?

⌦The graveyard — where signal goes to die

Most people only want the signals that work. Understanding why the rest don't IS the skill.

A signal dies two fundamentally different ways. Knowing which is which is the whole skill.

Death A — real signal, no edge left

Over-analyzed (price & chart patterns — every market, including crypto). The signal is completely real. It's also the most-used input on earth, so the edge is competed away almost instantly. Real pattern, ~zero remaining alpha. This is why our Screen 01 lead-lag died — not because the pattern is fake, but because everyone already trades it.

Out-competed (equity stat-arb, latency-gated signals). The edge is real — and already harvested by insanely-funded quant teams with better data, faster pipes and more capital (Renaissance, Citadel, Two Sigma). Not impossible; effectively not ours. If extracting it needs speed or scale we don't have, it isn't our edge.

Decayed after publicity (the half-life problem). Congressional-trade copying — the "Pelosi tracker" — genuinely worked: disclosed trades from informed actors, copyable for free. Then trackers, headlines and ETFs (NANC/KRUZ) crowded in and compressed it. The signal stayed real; its edge ran out of half-life.

Death B — there was never a signal

The in-sample mirage (overfitting). A rule that looks gorgeous on history and dies on data it was never fit on — because there was never an edge, only noise that happened to fit the past. Live example: Lab-log Screen 01, in-sample Sharpe +0.82 → out-of-sample −0.59. The ONLY genuinely "fake" category — and the most dangerous, because it's the most seductive.

⌦ The headstones — signals we tested out-of-sample and buried

41 hypotheses tested · 0 deployable edges — public + academic claims, our own proprietary on-chain data, and even one signal that looked real until a deeper cut buried it (above). And our tester is calibrated: it confirmed a known-true equity anomaly, so the kills are credible — not the artifact of an always-negative test. The graveyard grows as we test more. A record of honest kills is rarer — and more trustworthy — than another channel shouting buy.

Order of proof is non-negotiable: backtest → private forward-proof → public track record → charge.